Key Takeaways

Debt ceiling and AI investments dominated the market after the banking sector stabilized.

The US outperformed the rest of the world at 8.39% and took the lead as the best performing market of the past 12 months.

Treasury yield increased across all the maturities pushing US bonds to -0.84% loss.

Inflation dropped to 3% year-over-year; significant improvement compared to 9.1% just 12 months earlier in June 2022.

No recession yet, as GDP is expected to grow at 2.3% in Q2.

Market review

After a good stock market performance in the first quarter, second quarter marked the start of new bull market as stocks grew more than 20% from the last year lows. Relief came after the US avoided default by increasing the debt ceiling in June, while big tech companies continued to benefit from the enthusiasm surrounding anything AI related. This helped US stocks do better than international ones and returned 8.39% compared to 3.03% of developed markets and 0.9% of emerging markets[1]. As can be expected given these results, VanderPol Investments’ (VPI) best performing fund of the quarter was Dimensional US Core Equity Market ETF which returned 8.1%. With equity ownership of over 2,400 US companies the goal of this fund is to be the main source of growth in our portfolios over the long term. Looking at individual countries, the best performance was Greece with 25% gain and the worst one was Turkey with more than -10% loss[1].

Market Performance [Source: Quarterly Market Review - Second Quarter 2023 by Dimensional Fund Advisors] [2]

The worst performing asset class of the 2nd quarter are commodities, where BCD, a commodity fund used by VPI lost -3.5%[3]. Even though exposure to commodities was a drag on the overall performance this time, we continue to believe that potential long-term benefits of commodity allocation outweigh short-term losses. The low correlation with other investments and their potential to partially hedge inflation when commodity prices start to rise, can help offset losses in other investments. A recent example of this benefit is the fact that BCD is the best 3-year performing fund among our investments at an annual return of 20%[3].

Diving deeper into the stock market, smaller companies (average market capitalization $2.8 billion[4]) underperformed the large ones (average market capitalization $621 billion[5]) and the more expensive ones with higher growth expectations outperformed the cheaper ones. As the gap in performance between the largest companies and the rest of the market grows (charts below), the risk of high portfolio concentration by staying in pure market-based index becomes larger.

Stock performance of S&P 5 vs S&P 500 by Axios [Source: https://www.axios.com/2023/06/01/sp500-tech-companies-stock-price]

As of end of quarter, more than 22%[6] of the S&P 500 index comprised of just 5 of its biggest companies, a concentration on par with recent peak in 2020 and higher than previous maximum of 17.4% in 1982[7]. Having a diversified portfolio based on fundamental stock selection process with tilt towards smaller, more profitable, and cheaper companies, VPI helps to reduce concentration risk in the portfolios to just 12% of the top 5 biggest companies[8].

Fixed Income

We are on the heals of the worst-ever year for U.S bonds in 2022. It is easy to get confused about bonds falling in value, and what that really means for your portfolio. First, we want to look at general bond pricing and how it reacts to market conditions. Then, we want to touch on what the current economic environment means for bond prices in the future.

To start, lets look at the components of a bond:

1. Face Value: money amount the bond is worth at maturity.

2. Coupon Rate: rate of interest the bond issuer will pay on the face value of the bond.

3. Coupon Dates: the dates on which the bond issuer will make interest payments.

4. Maturity Date: date when the bond will mature, and the issuer will pay the face value.

When a bond is issued at the face value with a specific coupon date, the issuer is required to pay that coupon until the maturity date of the bond. If you bought a 10-year U.S Treasury bond on June 30, your coupon rate would have been 3.81%. If you hold that bond until maturity, you are guaranteed to get your principal back plus interest; however, a bond does not have to be held to maturity.

Just like stocks on the New York Stock Exchange, the price of bonds change on a daily basis in the open market. The price of a bond changes in response to a change in interest rates. As you have possibly heard, bond prices are inversely affected by interest rates. When interest rates go up, bond prices fall. When interest rates go down, bond prices rise. If there is a bond out there that has a coupon rate of 2%, and interest rates go up to 3%. The price of that bond needs to go below face value. The drop in price allows the yield on the bond to go up, in order to be comparable to the newly issued bonds in the market.

Looking at 2022 and early 2023, the Fed implored aggressive interest rate hikes, which in return resulted in bond prices falling. As we point out in this market report, inflation looks to be stabilizing. This is a sign for interest rates to start coming down, which would raise bond prices.

After bond yields fell during the first quarter as a reaction to banking turmoil in March, the second quarter saw a reversal when the market stabilized. This quarter the yields on bonds increased slightly for all the maturities, reaching up to 5.24% on 1-year treasuries and 3.81% on 10-Year Treasury Bond. This increase in yields pushed down the prices and US bonds returned negative -0.84% past quarter[9].

10-Year Treasury Rate [Source: https://ycharts.com/indicators/10_year_treasury_rate]

VPI understands the complexity of bonds, and fixed income. If you have any questions, please don’t hesitate to reach out.

Economy

The Fed started increasing interest rates last year to cool down the inflation, as slowing down the economy seemed to be necessary to achieve any progress. While the stock market reacted quickly to prospect of high interest rates and slow economy, the economy itself took bit longer to show how big the jump in interest rates really was. After the slow down of housing market last year, in March of this year we learned how quickly a bank can collapse thanks to the Silicon Valley Bank. Despite the fact that banking turmoil continued in the second quarter when First Republic Bank’s failure required its takeover by JPMorgan in May, the overall situation seem to be stabilized and is not a major concern for market right now. Improvement on the inflation front last couple months helped to calm down the market too, as the report for June showed 3% year-over-year growth in June, only a third of 9.1% just one year earlier in June 2022[10]. Other key economic indicators like Real Personal Consumption, Employment, and Industrial Production, continue to trend upward but at slower pace as signs of decreasing labor demand are present[11]. The pace of adding new jobs slowed down to the average of 244,000 in Q2 from 312,000 in Q1 while the average weekly hours dropped to 34.37 in Q2 from 34.50 in Q1[12]. Overall, the most recent employment report for June showed unemployment rate changed little at 3.6% with employment trending up the most in government, and health care[13]. Based on the current projections the US GDP is expected to grow faster at 2.3%[14] in Q2 after reaching 2.0% in Q1[15], slowly increasing the chances of no recession in 2023.

Key Economic Indicators with cumulative growth by Morningstar [Source: US Economic Pulse: June 2023 by Morningstar]

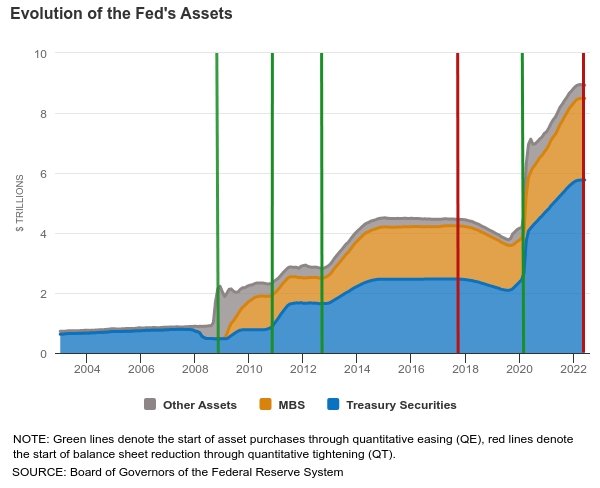

The upper range of Fed rates increased from 5% to 5.25% in May, and stayed unchanged during the following meeting in June, as the Fed is waiting to see fully the delayed effect of the current interest rates on the overall economy. While the interest rates are slowly approaching their expected peak, the shrinking of the balance sheet is expected to continue for some time. The total assets of the Federal Reserve were down this July to $8,298 billion from the peak of $8,965 billion back in April 2022[16]. At the current pace, Fed intends to reduce it’s holding by $95 billion per month[17].

Fed balance sheet [Source: https://www.richmondfed.org/publications/research/econ_focus/2022/q3_federal_reserve]

Future with AI

Markets and the investors are often the first ones exposed to new and emerging technologies. While the excitement of great returns can tempt someone to quickly change their investments to not miss out on the big gains, staying the course of your long-term plan can often save you from anxiety and risks that are associated with chasing the new “shiny” thing of the day. Do you feel like your long-term plan needs a touch up or are you just curious where you stand on your journey? Let us know, we are more than happy to help!

Authors: Noah Hoekstra and Richard Toth, CFA, CAIA

References

[1] Source: Quarterly Market Review – Second Quarter 2023 by Dimensional Fund Advisors

[2] US Stock Market (Russell 3000 Index), International Developed Stocks (MSCI World ex USA Index [net dividends]), Emerging Markets (MSCI Emerging Markets Index [net dividends]),Global Real Estate (S&P Global REIT Index [net dividends]), Commodities (The Bloomberg Commodity Total Return Index), US Bond Market (Bloomberg US Aggregate Bond Index), Global Bond Market ex US (Bloomberg Global Aggregate ex-USD Bond Index [hedged to USD])

[3] Source: Morningstar

[4] Represented by Russel 2000 as of 6/30/2023 [Source: https://www.ftserussell.com/products/indices/russell-us]

[5] Represented by Russel 1000 as of 6/30/2023 [Source: https://www.ftserussell.com/products/indices/russell-us]

[6] Top 5 holdings based on iShares Core S&P 500 ETF

[7] Source: https://www.spglobal.com/marketintelligence/en/news-insights/latest-news-headlines/top-5-tech-stocks-s-p-500-dominance-raises-fears-of-bursting-bubble-59591523

[8] Based on Morningstar’s Stock Intersection Report of VPI’s all stock model portfolio

[9] US Bond Market (Bloomberg US Aggregate Bond Index)

[10] Source: U.S. BUREAU OF LABOR STATISTICS

[11] Source: US Economic Pulse: June 2023 by Morningstar

[12] Source: Current Employment Statistics - CES (National) by U.S. BUREAU OF LABOR STATISTICS

[13] Source: U.S. BUREAU OF LABOR STATISTICS

[14] As of 7/13/2023 [Source: https://www.atlantafed.org/cqer/research/gdpnow]

[15] Source: https://www.bea.gov/news/2023/gross-domestic-product-third-estimate-corporate-profits-revised-estimate-and-gdp-industry

[16] https://www.federalreserve.gov/monetarypolicy/bst_recenttrends.htm

[17] https://www.federalreserve.gov/newsevents/pressreleases/monetary20220504b.htm

Disclosures

VanderPol Investments, LLC (“VPI”) is a registered investment adviser located in Michigan. VPI may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements.

This presentation is limited to the dissemination of general information regarding VPI’s investment advisory services. Accordingly, the information in this presentation should not be construed, in any manner whatsoever, as a substitute for personalized individual advice from VPI. Information presented is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and unless otherwise stated, are not guaranteed. Be sure to first consult with a qualified financial adviser and/or tax professional before implementing any strategy discussed herein. Any client examples were hypothetical and used to demonstrate a concept.

Past performance is not indicative of future performance. Therefore, no current or prospective client should assume that future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended by VPI), or product referenced directly or indirectly in this presentation, will be profitable. Different types of investments involve varying degrees of risk, & there can be no assurance that any specific investment or investment strategy will suitable for a client’s or prospective client’s investment portfolio.

Various indexes were chosen that are generally recognized as indicators or representation of the stock market in general. Indices are typically not available for direct investment, are unmanaged and do not include fees or expenses. Some indices may also not reflect reinvestment of dividends.

VPI may discuss and display, charts, graphs, formulas which are not intended to be used by themselves to determine which securities to buy or sell, or when to buy or sell them. Such charts and graphs offer limited information and should not be used on their own to make investment decisions.